Tax Resolution Services

Tax resolution services assist individuals and businesses in settling disputes or unpaid debts with the IRS

Offer in Compromise (OIC)

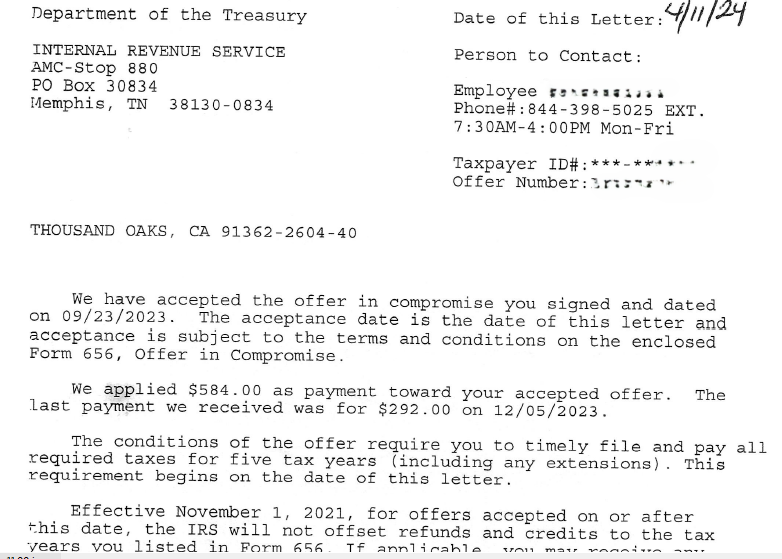

An Offer in Compromise (OIC) allows qualified taxpayers to settle tax debt for less than the full amount owed when paying in full causes financial hardship or is unlikely. Qualification is based on the taxpayer's individual circumstances.

Key Features:

- Stops Aggressive Collection Activity: Collection actions are paused while the offer is pending.

- Flexibility: Not locked into monthly payments.

- Compliance Monitoring: The IRS closely monitors future tax compliance.

- Default Risk: Tax debt can be reinstated if the taxpayer defaults on the agreement.

- Financial Scrutiny: Taxpayer must undergo a detailed financial analysis.

Partial Pay Installment Agreement (PPIA)

Partial Payment Installment Agreements (PPIA) allow taxpayers to make reduced monthly payments on their tax debt based on their current financial situation. Once accepted by the IRS, and provided that taxpayers continue to make timely monthly payments, they may be able to settle their debt for less than the full amount owed. Taxpayers must continue to file and pay all future taxes on time.

Key Features:

- Stops Aggressive Collection: Halts wage garnishments, bank levies, and harassing collection calls.

- Compliance Required: Taxpayers must file and pay future taxes on time to maintain status.

- Requires Financial Analysis: Taxpayers must submit detailed Collection Information Statement (CIS).

- Less negotiation time: Generally accepted faster than an Offer in Compromise

- Does Not Toll the CSED: The Collection Statute Expiration Date (CSED) continues to run while in PPIA status.

Currently Not Collectible

Currently Not Collectible (CNC) allows qualified taxpayers to suspend active collection activities. While in CNC status, the taxpayer is not required to make payments on the tax debt. The IRS will review financial information—including monthly income, expenses, and assets—to determine if payment would cause significant hardship. While the tax debt does not go away, this status prevents the IRS from issuing new

levies or seizing income and property.

Key Features:

- Requires Financial Analysis: Taxpayers must submit detailed Collection Information Statement (CIS).

- Stops Aggressive Collection: Halts wage garnishments, bank levies, and harassing collection calls.

- Compliance Required: Taxpayers must file and pay future taxes on time to maintain status.

- Interest/Penalties Accrue: Penalties and interest continue to build up, and the collection statute of limitations keeps running.

Frequently Asked Questions

How to get an offer in compromise approved?

It's best to hire a licensed Enrolled Agent who has experience negotiating with the IRS. Provide the requested documentation.

How much should I offer in compromise to the IRS?

Every case is different. The offer amount depends on your tax analysis and financial analysis.

What happeneds if I file taxes late?

All taxes must be filed before any resolution is established. We will file any unfiled taxes. The IRS will charge a penalty for late taxes.

Can you have two payment plans with the IRS?

No, you can only have one payment plan with the IRS.

How much interest does the IRS charge on a payment plan?

The interest rate is adjusted quarterly, and compounded daily. Interest will accrue on any unpaid tax, penalties and interest until the balance is paid in full. The IRS uses the federal short-term rate based on daily compounding interest. Changes to the rate don't affect the interest rate charged for prior quarters or years.

How long can I stay in Currently Non Collectible (CNC)?

You remain in CNC as long as you remain unable to pay.